Will We Enter a Post-Democracy World?

"No one pretends that democracy is perfect or all-wise. Indeed, it has been said that democracy is the worst form of Government except all those other forms that have been tried from time to time."

--Winston Churchill

It's been a rough few years for democracy. Despite that, Westerners always seem to assume that the most highly evolved form of government is democratic. The trouble with that notion is that, at some point, a majority of voters realize they can vote for politicians who promise them the most stuff, regardless of whether or not it is good policy or financially sustainable. And once that occurs, the country is (perhaps irreversibly) on a pathway to decline.

Take Greece, for example. Even though it isn't the sole (or even largest) cause of the Eurozone crisis, it stands as an example of a poorly governed nation that lived far beyond its means for years. Tax evasion was rampant, and when the credit card bill arrived in the mail, the Greeks couldn't pay up. They sought a bailout, and the austerity imposed upon them appears to have made matters even worse.

In short, an irresponsible, democratically elected government in Greece had to turn to unelected officials to get something drastic done (even if that solution is far from perfect). Greece's fate is now in the hands of non-Greeks: Angela Merkel and unelected bureaucrats in the troika -- the European Union, International Monetary Fund and European Central Bank.

Events like this have had a pernicious effect on how Europeans view the EU. One Charlemagne column in The Economist describes how the EU suffers from a legitimacy problem because of a democratic deficit. Many of the movers and shakers are unelected or too far removed from the citizens they represent. Charlemagne summarizes the problem:

The EU boasts of being a union of democracies. But its crisis of legitimacy is intensifying as it delves more deeply into national policies, especially in the euro zone. One problem is the evisceration of national politics: whatever citizens may vote for, southerners end up with more austerity and northerners must pay for more bail-outs. Another is that the void is not being filled by a credible European-level democracy.

In other words, regardless of what voters vote for, they get what leaders think is best.

But is that such a bad thing? As The Globalist reports, for two millennia, Europe considered democracy to be little better than "mob rule." The author, Zhang Weiwei, highlights four points to make his case:

(1) Democracies often elect untalented people; (2) the welfare state unaffordably increases in size; (3) consensus, and hence governance, is too difficult when minority parties are keen on obstruction; and (4) populism sacrifices long-term interests for the sake of short-term gains.

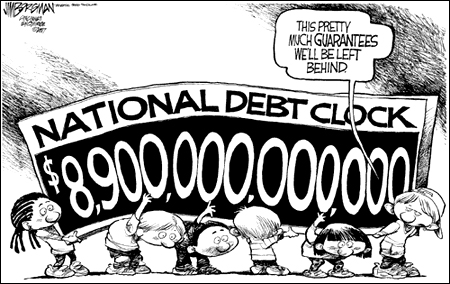

These criticisms aptly apply to the United States. Indeed, in 2011, we lost our AAA credit rating because our politicians had no good plan to reduce the national debt, and instead engaged in brinksmanship over raising the debt ceiling.

Similarly, Russians have flirted with democracy and free markets since the collapse of the Soviet Union. But, polls suggest that they wouldn't mind flipping the calendar back a few decades: 51 percent of Russians want a centrally planned economy and 36 percent believe the Soviet system was superior to what they have today.

Mr. Weiwei suggests that the world can learn from China, which chooses its leaders on a merit-based system. Of course, there's also a lot wrong with China, such as human rights abuses and a general lack of freedom.

Obviously, an entirely autocratic system is undesirable (and perhaps even evil), but it appears that a completely democratic one is, at best, dysfunctional. Is there a way, for the sake of economic prosperity, to strike a proper balance between the two?

(Parthenon: Steve Swayne via Wikimedia Commons)

{kind=link}